Table of Contents

Related Blogs

.avif)

%20(1).avif)

Employer-sponsored healthcare insurance has always been a cornerstone of the American healthcare system, with employees continuing to rank health benefits as one of their top priorities when choosing a job, even now in 2025. However, the issue is that traditional group coverage options have always been relatively expensive, especially for smaller employers looking to be competitive in today’s job market.

If this has been your experience when trying to keep up with traditional health benefits options, you’re not alone. In response to the needs and unique challenges facing firms of this size, the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) was established in 2017. With this type of HRA, companies with fewer than 50 employees who don’t currently offer a group health plan have an affordable, flexible way to contribute to their employees’ health care costs.

But in order for small businesses to reap the full advantages of a Qualified Small Employer HRA, employers must stay up-to-date with the contribution limits and rules set by the United States (U.S.) Internal Revenue Service (IRS) at the start of each year.

In this article, we’ll cover the QSEHRA contribution limits set for 2025 and other important rules to help you make the most of this HRA.

After reading, you’ll understand:

- The definition and purpose of a Qualified Small Employer Health Reimbursement Arrangement

- The 2025 limits for employer contributions into a QSEHRA plan

- Key rules and compliance requirements to maintain eligibility for a QSEHRA

- How a QSEHRA can provide advantages for your small business, particularly when combined with Direct Primary Care (DPC)

What is a Qualified Small Employer HRA?

The QSEHRA is a type of health reimbursement arrangement (HRA), which you can think of as a tax-advantaged employer-funded expense account that can be used to reimburse employees for eligible healthcare costs, including premiums on an insurance plan of their choice. Like the name suggests, the Qualified Small Employer HRA is specifically designed for any organization with less than 50 full-time equivalent (FTE) employees looking for an affordable way to offer small business medical benefits.

This can be a much more suitable alternative to traditional group health plans for smaller companies because it offers employers and employees greater financial control and customizability to fit their particular needs.

QSEHRA Reimbursement Process

Small employers can decide what they'll contribute to their employees’ health care costs, up to an annual maximum set by the IRS (see below). Employees pay their provider or insurance company for their health care costs, then submit proof of payment to be reimbursed by the QSEHRA using tax-free dollars up to their allowance amounts. While the employer is responsible for the reimbursement budget, an HRA administrator like Vitable, manages this process on the employer’s behalf, handling documentation, compliance, and disbursements.

To make it even easier, Vitable’s ICHRA debit card can be used to streamline eligible purchases, allowing employees to pay for healthcare expenses like therapy, prescriptions, fertility care, and more. It's a flexible, frictionless way for your team to use their benefits whenever and however they need them.

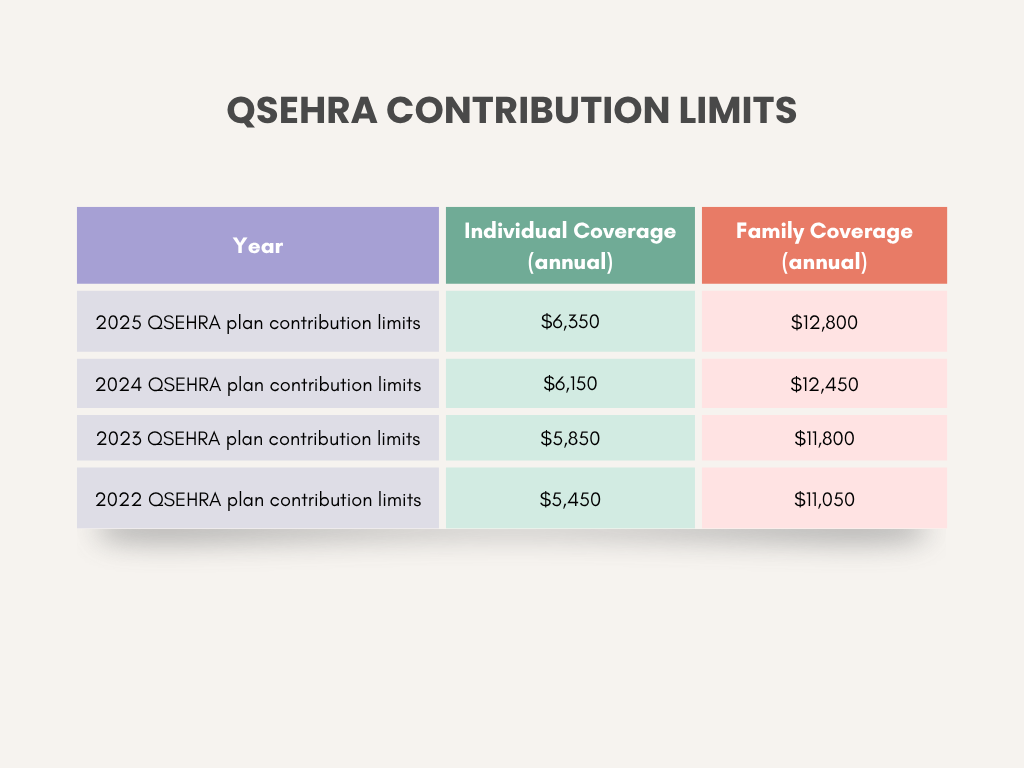

2025 Qualified Small Employer HRA Contribution Limits

In October 2024, the IRS published the 2025 limits for several types of benefit plans, including the QSEHRA plan, in their IRS Revenue Procedure 2024-40. For taxable years beginning in 2025, small employers can contribute up to:

- $6,350 yearly for single employees ($529.16 per month)

- $12,800 yearly for family coverage ($1,066.66 per month)

Although these limits represent the total amount of payments and reimbursements that can be offered through a QSEHRA, employers can also choose to set their contributions to be lower than the allowed maximum, depending on their budget.

Compared with 2024, the current limits represent a $200 annual increase (3.25%) for single employees and a $350 annual increase (2.81%) for family coverage. Overall, the annual QSEHRA employer contribution limits for both individuals and families have increased each year since 2022, as shown in the table below.

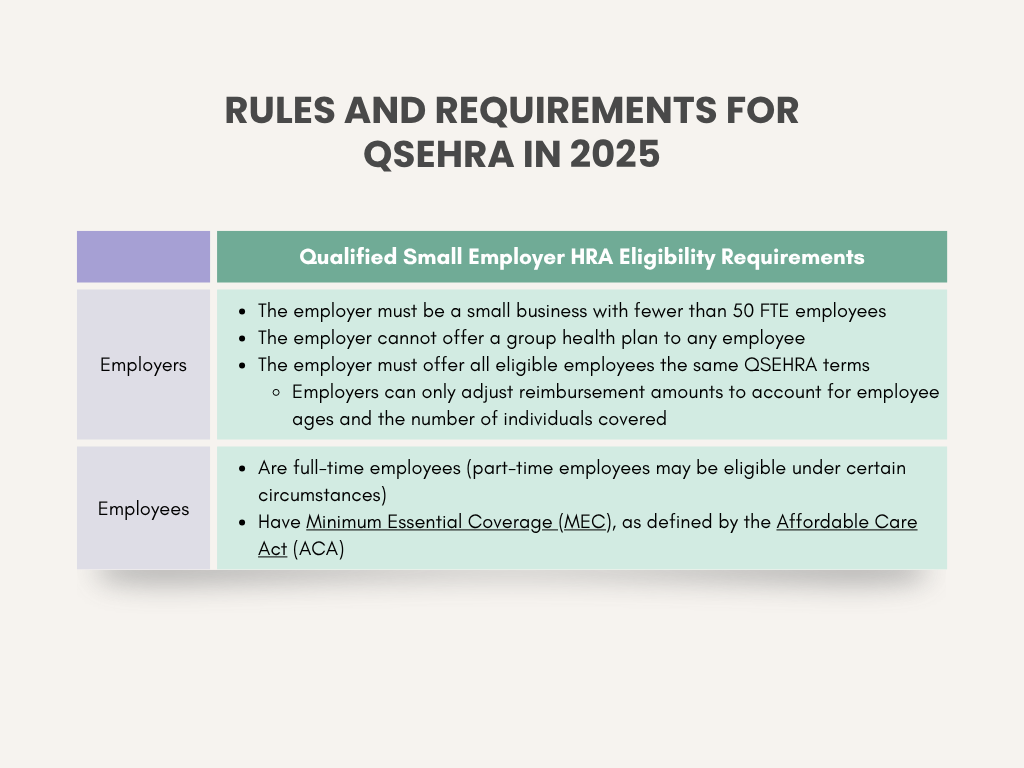

Rules and Requirements for QSEHRA in 2025

QSEHRA plans operate on a simple premise: employers reimburse, employees choose. To qualify for these small business medical benefits, the following rules and requirements must be met by small employers and their employees:

Employees must be enrolled in a health plan that meets Minimum Essential Coverage (MEC), as defined by the Affordable Care Act (ACA), in order to qualify for tax-free reimbursement through a QSEHRA because that’s what the IRS requires to maintain the tax-advantaged status of the benefit. MEC refers to a health insurance plan that meets the Affordable Care Act's (ACA) basic coverage requirements. This includes most employer-sponsored plans, individual plans purchased through the ACA Marketplace, and certain government programs such as Medicaid or Medicare.

Without MEC, any QSEHRA reimbursements the employee receives would be treated as taxable income, which defeats the purpose of using a QSEHRA to provide a tax-free benefit. Requiring MEC ensures that employees have a baseline level of health coverage while allowing employers to offer meaningful, tax-efficient support for their healthcare costs.

Examples of QSEHRA-eligible, tax-free reimbursements include:

- Monthly insurance premiums

- For individual ACA plans, Medicare Parts B and D, Medicaid (where premiums apply), dental or vision insurance, and—in some cases—a spouse’s group health plan (as a taxable benefit if the plan isn’t MEC)

- Prescription drugs and certain over-the-counter medicines (must be medically necessary; some may require a doctor’s note)

- Dental or vision coverage

- Preventive care services (e.g., screenings, immunizations)

- Mental health services

- Alternative treatments

- E.g., acupuncture, chiropractic care, dietitian or nutritionist services (if medically necessary), etc.

The ACA’s “Affordability” Requirement for a QSEHRA

What happens to premium tax credits with a QSEHRA? The answer to this question is that it depends. If an employer offers a QSEHRA that isn’t considered “affordable,” according to the ACA’s requirements, employees may qualify for a premium tax credit to lower the cost of Marketplace coverage that can be coordinated with the QSEHRA allowance.

For taxable years starting in 2025, an employer’s QSEHRA meets the ACA’s affordability requirements if the following criteria are met. The employee must not pay more than 9.02% of their household income on their portion of the insurance premium for the second-lowest-cost Silver plan (SLCSP) on the ACA Marketplace, after factoring in the QSEHRA allowance. Depending on whether your QSEHRA meets this requirement, one of two things can happen:

- The QSEHRA is considered affordable, and your employee is not eligible for any premium tax credits. They must use your company’s QSEHRA to help pay their premiums.

- The QSEHRA is not considered affordable, meaning your employee can use both their allowance and premium tax credits. However, before selecting a plan, the monthly QSEHRA allowance must be subtracted from the total tax credit subsidy to get the net amount that can be applied to cover the employee’s monthly premiums.

- This is required to ensure there is no “double-dipping” on tax benefits, which can carry hefty penalties from the IRS.

Visit this worksheet from the U.S. Department of Health and Human Services to find out if your QSEHRA meets the ACA requirements for “affordability.”

Key Compliance Considerations When Offering a Qualified Small Employer HRA

When choosing to offer a QSEHRA for your small business, employers must keep in mind some key compliance considerations to avoid risking non-compliance penalties.

- Required Written Notice to Employees: Employers offering a QSEHRA must provide written notice to eligible employees within at least 90 days prior to each new year (e.g., the upcoming 2026 plan year). If any employees are not eligible to participate at the time, they must receive written notice on the day that they do become eligible.

- Verify That Employees Have MEC: To be eligible for reimbursements through a QSEHRA, employees must provide proof that their health insurance meets MEC standards.

- There are two acceptable types of evidence:

- Official documentation from their insurance company (e.g., insurance card, description of benefits, or proof of coverage)

- The employee attests to their existing MEC, verifying the coverage start date and the name of the insurer

- There are two acceptable types of evidence:

- Meet Reporting Requirements for Reimbursements: The IRS requires employers to report QSEHRA on each eligible employee’s Form W-2, Wage and Tax Statement. This means disclosing the total reimbursement that the employee is entitled to throughout the year, not the amount they actually received during the year.

In addition to the above, employers must also ensure their set reimbursement amount doesn’t exceed the IRS annual maximums per employee. All employees must also receive the same reimbursement amounts (up to the annual maximum), unless they are eligible for more based on their age or coverage type (individual vs. family).

By ensuring these rules and requirements are all met, small employers can reap all the benefits of a QSEHRA while avoiding potential penalties from the IRS.

Tax Treatment for Employers and Employees with a Qualified Small Employer HRA

Employers: Reimbursements made through a QSEHRA are tax-deductible, which helps reduce your business’s overall tax liability.

Employees: As long as employees maintain MEC, their reimbursements are tax-free, meaning that money is not subject to income or payroll taxes. Learn more about MEC requirements under the ACA here.

These tax advantages usually apply to both federal and state taxes, but always check with a tax professional about your specific situation.

Benefits of Offering Small Business Medical Benefits Through a QSEHRA

Qualified Small Business HRAs were created as a creative solution for small businesses to offer affordable and flexible healthcare coverage for their employees. The table below outlines the several advantages that both employers and employees can gain by adopting a QSEHRA plan.

Overall, the QSEHRA is an excellent health benefits option for small business employers looking for flexibility and cost control to help them attract and retain top talent without offering more expensive traditional group health plans.

How Vitable Combines QSEHRA + Direct Primary Care in One Convenient Package

At Vitable, we’ve combined two powerful tools to create a unique solution for small businesses: QSEHRA and Direct Primary Care (DPC). Together, they help provide a simple, effective way for you to offer competitive health benefits in today’s job market.

Here’s how the combination works. QSEHRA serves to make insurance and medical expenses more affordable for employees, while a flat monthly DPC subscription gives your team unlimited access to primary care with no copays or deductibles. This means your team can get regular check-ups, preventative care services, free prescriptions, access to same/next day virtual visits from DPC providers, and so much more, without worrying about surprise charges.

The best part is that QSEHRA reimbursements help cover healthcare premiums on top of the excellent essential coverage that DPC already provides. Vitable also offers one-on-one support to help employees select the right insurance and employers choose reimbursement amounts within their budget.

You can also rest easy with straightforward health coverage when you combine Vitable’s QSEHRA and DPC plan. You’ll know exactly what you're paying in coverage each month, and by partnering with an experienced HRA administrator like Vitable, we handle all the complex paperwork and requirements so that you don’t have to! Plus, your business can potentially increase its cost savings and earnings long-term because this powerful combination helps keep your employees healthier and happier.

Meanwhile, our caring administration team will be with you every step of the way to keep things on track, from enrollment and compliance monitoring to reimbursement and reporting.

Discover more about the Vitable DPC model to learn how it works!

Ready for Better Health Benefits? Explore Vitable’s QSEHRA + DPC Offerings Today!

At Vitable, we understand that staying compliant isn’t just about meeting deadlines and following rules. Really, it’s about protecting your business and employees while fostering trust within your team. Our powerful QSEHRA plus DPC membership model offers easy-to-use health reimbursement accounts designed for small businesses, with convenient access to primary care providers that come with no copays, no deductibles, and no hassle. Your team gets quality healthcare when they need it without worrying about complex paperwork or unexpected bills, while you benefit from Vitable’s HRA administration expertise to keep your small business running smoothly.

Want to learn how we can create a small business medical benefits plan that works for your company’s unique needs? Contact a Vitable team member using the form below and get started offering better benefits today!

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.