Table of Contents

Related Blogs

.avif)

%20(1).avif)

As an employer, offering comprehensive and affordable health benefits is essential for attracting and retaining top talent. In 2022 alone, 43% of individuals who left their jobs cited poor benefits as their reason for doing so. However, finding the right solution that meets the diverse needs of your employees while staying within your budget can be challenging.

With more small to mid-sized businesses moving away from traditional health plans, companies are increasingly turning to alternative funding solutions to provide comprehensive benefits packages for their employees without breaking the bank. Navigating these options can seem complex and overwhelming, which is why Vitable Health has developed this employer guide to help you decide whether an individual coverage HRA (ICHRA plan) or a level-funded plan is right for your business. Read on to learn how these two types of plans compare, the benefits they provide, and which can help you deliver better healthcare benefits for your workers.

What is an Individual Coverage HRA (ICHRA)?

First introduced in 2020, an ICHRA is a structured health plan that can act as an alternative to a traditional group health insurance plan. An ICHRA plan enables companies of all sizes to utilize pre-tax dollars to reimburse employees for the cost of their individual health insurance premiums and potentially other eligible medical expenses. Individual coverage HRA plans are a type of HRA, which is an employer-funded plan that covers medical expenses for its employees. To learn about HRAs, including individual coverage HRAs, read our article here.

How does ICHRA health insurance work?

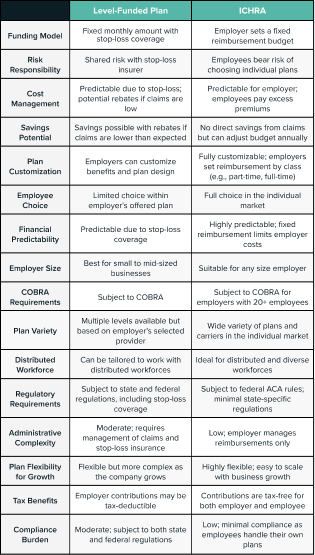

Employers that implement an ICHRA plan can choose how much they will contribute to the ICHRA for employee reimbursement. All workers within the same class (e.g., full-time vs. part-time) must receive the same contribution amount, although it may be increased by age or to accommodate those with more dependents.

Employees then purchase individual health insurance directly from a provider or through the Affordable Care Act (ACA) marketplace. Once an eligible medical expense or a health insurance premium (e.g., deductible or copayment) is incurred, the employee can request reimbursement with tax-free contributions from their employer through the ICHRA plan up to the amount spent.

Unlike employee-funded health savings accounts (HSAs) or Flexible Spending Accounts (FSAs), ICHRA funds cannot be withdrawn in advance to pay for medical expenses. An ICHRA also does not have a yearly reimbursement limit. It is important to note that only employees not currently enrolled in a traditional group health plan may be eligible for ICHRA health insurance. Read more here to learn about ICHRA plans.

Key features and benefits

The standout advantage of ICHRA is its flexibility. Employers control costs by setting a fixed reimbursement amount, which can be adjusted annually. This structure reduces administrative burdens by eliminating the need for claim management or provider negotiations. Employees benefit from the ability to choose health plans based on personal preferences, geographic location, and healthcare needs. This is particularly advantageous for distributed teams, where employees in different regions can select plans that best suit their local healthcare providers and needs.

Additionally, ICHRA is an appealing option for businesses new to offering health benefits, as it eliminates participation requirements and provides full control over reimbursement limits and eligible expenses.

Eligibility and enrollment

To participate, employees must have individual health insurance or Medicare. Employers can determine eligibility based on employee classes such as full-time, part-time, or regional workers. The ability to create tailored reimbursement plans for different employee categories ensures that all workforce segments are covered appropriately. Enrollment is simple, requiring employees to submit proof of coverage and qualifying expenses for reimbursement. Employees may also remain eligible for premium tax credits, though these are reduced by the ICHRA contribution.

What is a Level-Funded Health Plan?

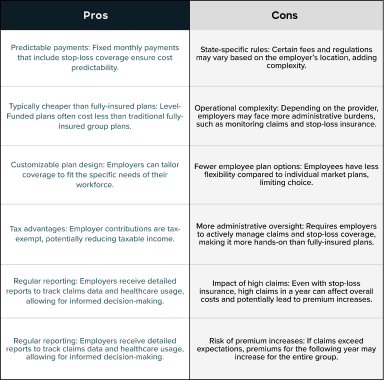

Level-funded plans are designed to be a hybrid between fully insured and self-funded plans. Employers pay a fixed monthly premium to manage high claims, which covers the maximum claims liability, administrative fees, and are often paired with stop-coverage. Stop-coverage, also known as stop-loss insurance, protects self-insured businesses against unexpectedly high medical costs.

In a traditional health plan, the insurance carrier assumes all financial risk of covering the employees’ medical claims; however, level-funded plans partially transfer this burden to the employer, making it more cost-effective in comparison. Additionally, they provide flexibility in plan design, allowing businesses to tailor coverage to meet the specific needs of their employees.

Regulatory framework

Level-funded plans are regulated under the Employee Retirement Income Security Act (ERISA), similar to self-funded plans. This federal oversight allows for greater flexibility in plan design than fully insured plans, which are subject to state insurance regulations. Employers offering level-funded plans must comply with ERISA's reporting and fiduciary requirements, including providing Summary Plan Descriptions (SPDs) and filing Form 5500. Additionally, level-funded plans must adhere to federal mandates like the Affordable Care Act (ACA), ensuring essential health benefits and preventive services are covered, while stop-loss insurance is regulated at the state level.

Eligibility and enrollment

Level-funded plans are typically available to small and mid-sized businesses, though eligibility criteria can vary by provider. To qualify for these plans, employers must meet specific requirements, such as a minimum number of enrolled employees, often around ten or more. Enrollment involves selecting a plan structure, determining contribution levels, and providing employee census data for underwriting purposes. Unlike traditional fully insured plans, level-funded plans may require health questionnaires or claims history to assess risk. Once enrolled, employees choose from available coverage options, similar to traditional group health plans, but with the potential for cost savings and refunds.

Comparing an ICHRA Plan vs. Level-Funded Health Plans: Which is Right for You?

ICHRA and level-funded health insurance plans offer distinct advantages, depending on employer size and financial risk tolerance.

Individual Coverage HRA: Key Advantages and Considerations

Cost control for employers

One of the key advantages of ICHRA is that it grants employers considerably more flexibility and cost control. Employees can choose the amount they wish to contribute to an ICHRA, based on their financial capabilities, either as a fixed dollar amount or as a percentage of their premiums. Unlike other types of HRAs, an ICHRA plan has no contribution limits and no minimum employee participation requirements.

Freedom of choice for employees

Unlike other forms of health plans, ICHRAs are unique in that they can reimburse an employee’s health insurance premiums, offering them the freedom to select their preferred coverage plan. Rather than being limited by a company-selected one-size-fits-all health benefits package, an ICHRA plan enables employees to explore the entire market and select a plan that aligns with their unique needs, preferences, and budget.

Tax advantages for employers and employees

All reimbursement contributions made by the employer into an ICHRA are tax-deductible and not considered part of wages, resulting in potential long-term savings. Any additional contributions made by employees also use pre-tax dollars, reducing both the employer's and employees' overall tax liability.

Compliance with the Affordable Care Act (ACA)

An ICHRA can be considered a replacement for the traditional group health plan because it meets all the Employer Mandate requirements imposed by the US ACA. By offering an Affordable ICHRA, employers can provide a customizable ACA-compliant health plan with comprehensive benefits to their full-time and part-time employees.

Level-Funded Health Plans: Key Advantages and Considerations

Stable cost structure

The key difference between ICHRAs and level-funded plans lies in the cost structure. Unlike an ICHRA plan, which transfers financial responsibility for coverage choice to employees, level-funded plans involve a shared financial risk between the employer and the insurance carrier.

With the fixed monthly cost, employers with budget limitations can benefit from the predictability of these plans. However, level-funded plans ultimately require more oversight, and if claims are too high, the employer’s stop-loss insurance premiums can rise, increasing overall costs over time. In contrast, if annual employee medical claims are lower than expected, employers are eligible for a surplus refund at the end of the year.

Scalability and customization

Another similarity between ICHRAs and level-funded plans is that they offer adaptability as a business evolves. The company’s workforce and healthcare needs may change as it undergoes growth, and under both types of plans, employers have the option to adjust coverage levels and costs to align with these changes. Although level-funded plan premiums do not offer the same simultaneous tax benefits as ICHRA health insurance does.

Opportunities for employee wellness benefits

There is the option to combine level-funded plans with HRAs to cover specific costs, like fertility, allowing for a flexible, capped structure without committing to extensive health benefits upfront. Additionally, these types of health plans often come with access to wellness programs and preventative care initiatives.

There is also a unique type of ICHRA offered by Vitable that provides similar access to comprehensive preventative care services at affordable prices, enabling employers to reduce overall healthcare costs and enhance productivity long-term.

Vitable’s ICHRA-DPC Plans: Affordable, Flexible Healthcare Benefits for Hourly Workers

As an affordable health benefits platform, Vitable offers flexible ICHRA options for employers, including enhanced benefits for part-time and hourly workers, through our innovative Direct Primary Care (DPC) membership. This type of health plan offers the best of both worlds, combining the tax benefits and customizability of ICHRAs with the predictability and wellness perks of level-funded plans. However, our ICHRA-DPC option eliminates the financial risk and hassle associated with level-funded plans.

Vitable’s DPC membership is a monthly subscription that requires no copays or deductibles from employees. Instead, for an affordable, fixed fee paid by the employer, members receive a variety of primary care benefits. This includes unlimited primary care visits, access to same-day appointments, mental health services, free prescription medications, and more.

Combined with our ICHRA plan, Vitable enables you to provide better primary healthcare to your team, while empowering employees to select and obtain their preferred health insurance coverage independently. To learn more about DPC and how these memberships work, click here.

Leverage Vitable’s HRA Administration Expertise for Better, Smarter Benefits

Keeping up with the changing health insurance market, from navigating jargon to understanding nuances between different plans, can be unnecessarily complex, but Vitable’s HRA administration expertise can help!

Vitable offers a comprehensive solution for employers seeking to provide affordable healthcare benefits to their workers. As an experienced HRA administrator, we streamline the entire process of implementing and managing ICHRA plans, handling everything from enrollment and claims processing to ensuring compliance with federal regulations. From setup and compliance to employee education and claims processing, Vitable ensures the day-to-day oversight of your ICHRA health insurance plan runs smoothly, enabling you to focus on your business.

Conclusion

Choosing between an ICHRA plan and a level-funded health plan for your business will require careful consideration of several factors, depending on your organization’s size, financial capabilities, and employee needs. Although both types of plans have their unique advantages, many employers may find that ICHRAs are a better overall fit due to their greater flexibility and tax benefits. Businesses that implement these plans can also take advantage of expert HRA administration services from partners like Vitable to make this process even more hassle-free. Overall, this guide can help employers identify the key differences between ICHRA health insurance and level-funded plans, enabling you to implement a health benefits solution that best suits both your business and your employees' healthcare needs.

Built for Better: How Vitable is Setting the New Standard for Better Health Benefits

Looking for a smarter solution to better health benefits at affordable prices for your business? Vitable is revolutionizing the approach to insurance and primary care. Our innovative combination of DPC memberships and ICHRA plans delivers comprehensive, accessible, high-quality healthcare benefits for hourly workers without breaking the bank.

Why Choose Vitable?

- Flexible ICHRA options tailored to your business size and needs

- Affordable monthly DPC subscriptions for quality primary care with no hidden fees

- Cost-effective solutions that don't compromise on care quality

- Easy, hassle-free HRA administration with seamless implementation

Vitable’s HRA experts make it easy for you to design the best HRA plan for your business. Take the first step towards better health benefits—schedule your free consultation with us to explore your ICHRA and DPC options!

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.