What is an Applicable Large Employer (ALE)?

If you're a small business owner, startup, or growing company trying to determine whether you’re required to provide health benefits under the Affordable Care Act (ACA), the first step is figuring out if your organization is considered an Applicable Large Employer (ALE).

Determining ALE status can feel confusing, especially if your workforce includes a mix of full-time, part-time, and seasonal employees. So, how do you know if your company qualifies?

In this guide, we'll walk you through what defines an Applicable Large Employer, how to calculate your ALE status, and what ACA requirements you'll need to meet if you qualify.

What is an Applicable Large Employer (ALE) and Why Does It Matter for ACA Compliance?

Under the ACA, not every business is required to offer employee health coverage. To focus compliance requirements on companies large enough to manage them, the ACA sets a clear threshold: the Applicable Large Employer (ALE) standard.

An ALE is a company that averaged 50 or more full-time employees or full-time equivalents (FTEs) during the previous calendar year.

Being classified as an ALE matters because it triggers specific ACA compliance obligations. If you meet the ALE criteria, you are legally required to provide health coverage that meets ACA standards and to properly document your compliance. Failure to meet these requirements could expose your business to expensive IRS audits and significant penalties.

How to Determine If Your Business is an ALE

Determining your ALE status isn’t just about counting how many employees are on your payroll. The ACA sets specific rules for how different types of workers—full-time, part-time, seasonal, and others—must be counted toward your total. Here’s how the calculation works for each group:

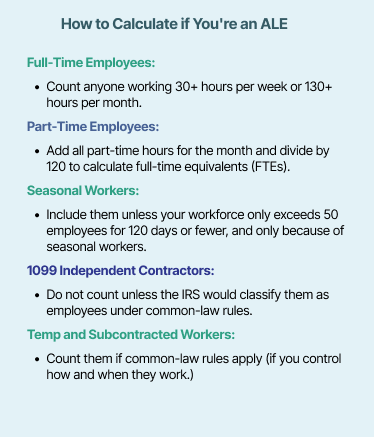

Full-Time Employees

According to the ACA, a full-time employee is someone who works 30 hours or more per week, or 130 hours in a month. Each person who meets that standard counts as one full-time employee for that month, regardless of the duration of their employment during that period. Even if someone is only employed for part of the month, if they reach 130 hours, they must be included in that month’s ALE calculation.

If you have 50 or more full-time employees, you are automatically considered an ALE. If you have fewer than 50 full-time employees, your full-time equivalent (FTE) employees may still push you over the 50-mark (more on this below).

Part-Time Employees (Calculated as Full-Time Equivalents)

Part-time employees—those who work fewer than 30 hours per week—are still factored into your ALE determination through a calculation called full-time equivalents (FTEs).

What is a full-time equivalent (FTE)?

The IRS defines a full-time equivalent employee as a combination of employees, each of whom individually is not a full-time employee, but who, in combination, are equivalent to a full-time employee.

How to calculate FTEs:

- Add up all the hours worked by part-time employees during the month (capping each individual employee at 120 hours).

- Divide the total part-time hours by 120.

Example:

If your part-time staff worked a combined 1,200 hours in a month, that equals 10 FTEs

- 1,200 ÷ 120 = 10 FTEs

Important: Full-time employees and FTEs are added together each month to determine your ALE status.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.

Seasonal Employees

Seasonal employees are generally counted toward your ALE determination just like full-time or part-time employees:

- Any seasonal employee who works 130 hours or more in a month is considered a full-time employee for that month.

- If a seasonal employee works fewer than 130 hours in a month, their hours are included in your full-time equivalent (FTE) calculation.

However, the ACA provides a seasonal worker exception that may apply in certain cases.

According to the IRS, if your company has more than 50 full-time (or FTE) employees for 120 days or fewer during the year, and the increase is entirely due to seasonal workers, you may not be considered an ALE under the ACA.

Why does the seasonal worker exception exist?

Congress and the IRS recognized that some businesses, like farms, retailers, hospitality companies, etc., only need extra employees for short, predictable periods (like harvest season, holidays, or summer tourism).

If seasonal labor pushed those businesses above the 50-employee threshold for just a short period (defined as 120 days or fewer), it would unfairly penalize them and force them to meet year-round employer mandate requirements, even though their normal business model doesn't sustain a large workforce year-round.

1099 Independent Contractors

Workers who receive a Form 1099-NEC are classified as independent contractors and are not included in your ALE calculation, since they’re not considered employees under the ACA.

However, if a contractor is working under conditions similar to an employee (for example, if you control their schedule, work method, or provide their tools), the IRS may consider them a common-law employee. If that’s the case, they should be included in your ALE calculation.

Subcontracted Employees

If your business utilizes staffing agencies, subcontractors, or temp services, your obligation to count their hours depends on whether or not you meet the IRS’s criteria for a common law employer.

Under the IRS common law rules, you are considered an employer if you:

- Direct the individual’s daily activities,

- Determine how and when the work is performed,

- Provide necessary tools or equipment.

Even if the worker is on someone else’s payroll, if you exercise significant control over how and when they work, the IRS may require you to include them in your ALE calculation.

Calculating Your ALE Status: Step-by-Step

Once you’ve determined your full-time employees and full-time equivalents (FTEs), the final step is to calculate your average over the entire year.

Here’s how to do it:

- Add the total number of full-time employees and FTEs for each month.

- Add the monthly totals together for all 12 months.

- Divide the total by 12 to find your average.

If the result is 50 or more, your business is considered an ALE for the current year.

Example:

Let’s say your monthly numbers look like this:

- January–March: 20 full-time employees + 25 FTEs = 45 employees

- April–December: 30 full-time employees + 30 FTEs = 60 employees

Step 1: (45 employees × 3 months =135) + (60 employees × 9 months =540)

Step 2: 135 + 540 = 675 for the year

Step 3: 675 ÷ 12 months = 56.25 avg. employees for the year

Result: You would be classified as an ALE.

Understanding ACA ALE Requirements

Now that you know how to calculate whether your business qualifies as an Applicable Large Employer (ALE), it’s important to understand the responsibilities that come with it. As an ALE, you must meet specific ACA ALE requirements to stay compliant and avoid costly penalties.

Here are the four main requirements every ALE must follow:

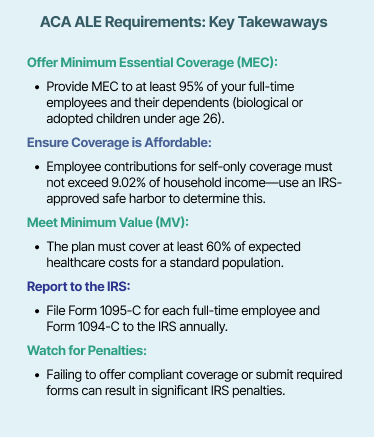

1. Offer Minimum Essential Coverage (MEC)

You’re required to offer Minimum Essential Coverage (MEC) to at least 95% of your full-time employees and their dependents, which includes biological or adopted children under the age of 26. It’s important to note: coverage for spouses is not required under the ACA, but is commonly offered.

MEC refers to a base level of health coverage that includes essential services, such as:

- Preventive and wellness care

- Outpatient services

- Emergency care

- Hospitalization

Keep in mind that limited plans, standalone dental or vision coverage, or discount health programs are not considered MEC on their own. The coverage you offer must include comprehensive, core medical services to be ACA compliant.

2. Meet Affordability Standards

The ACA sets affordability standards to protect employees from paying too much for healthcare. For 2025, a plan is considered affordable if the employee’s share of the premium for self-only coverage doesn’t exceed 9.02% of their household income.

Because most employers don’t have access to their employees’ full household income, the IRS allows you to use one of three safe harbor methods to demonstrate affordability:

- W-2 Wages Safe Harbor: Based on what’s reported in Box 1 of the employee’s W-2.

- Rate of Pay Safe Harbor: Uses the employee’s hourly wage multiplied by 130 hours per month.

- Federal Poverty Line (FPL) Safe Harbor: Based on a fixed income amount tied to the federal poverty level for an individual.

These options allow you to determine affordability without requiring sensitive financial information from your employees.

3. Provide Plans That Meet Minimum Value (MV)

Employers must offer healthcare benefits that meet the ACA Minimum Value (MV) standard. In other words, the plan should cover at least 60% of the expected healthcare costs for a typical group of employees using standard medical services, such as:

- Doctor visits

- Hospital stays

- Prescription drugs

Even if your plan meets the MEC standard, it can still fall short of ACA requirements if it doesn’t meet Minimum Value, and that could lead to penalties.

4. File Annual Reports with the IRS

Each year, ALEs are required to submit two separate forms to demonstrate that they’re meeting ACA coverage and reporting requirements:

- Form 1095-C: Sent to each full-time employee. It outlines what coverage you offered, when it was available, and whether it met ACA requirements.

- Form 1094-C: This form is submitted to the IRS. It summarizes your workforce, including those who were offered coverage, and how you determined your ALE status.

The deadlines to submit these forms vary depending on whether you file by paper or electronically. Missing a deadline or submitting inaccurate information can result in penalties, even if you’re otherwise compliant. That’s why it’s a good idea to maintain organized and accurate records throughout the year. It makes reporting much easier and helps you stay in good standing.

Why Choose Vitable for ACA-Compliant Plans?

Understanding your responsibilities as an Applicable Large Employer (ALE) is the first step toward staying compliant with the ACA and avoiding unnecessary penalties. But navigating employer mandates and coverage requirements doesn’t have to feel overwhelming. Partnering with a trusted health benefits provider like Vitable can simplify the entire process.

Vitable is the health benefits platform designed to make healthcare better and more accessible for everyday workers. We believe affordable, high-quality healthcare should be within reach for every business and their employees. That’s why we make it easy for companies to offer better healthcare benefits while maintaining ACA compliance without breaking the bank.

Whether you need an affordable MEC plan or are looking for access to major medical at a fraction of the typical cost through Health Reimbursement Arrangement (HRA) plans, Vitable offers flexible, compliant solutions built for today’s workforce.

Every Vitable plan includes our enhanced Primary Care membership, providing your employees with meaningful, affordable access to care, including:

- Unlimited primary care visits

- Free dependent coverage

- Access to 1,000+ prescriptions

- Mental health services

- Same-day appointments

- And more!

With Vitable, you can offer better benefits, support employee satisfaction and retention, and meet ACA requirements—all at a cost that works for your business.

Ready to start offering better benefits?

Contact Vitable today to learn how we can help you simplify compliance, control costs, and deliver healthcare your workforce will value. Book a call.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Vitable helps employers provide better healthcare to their employees and dependents by improving accessibility, cost, and quality.