Table of Contents

Related Blogs

.avif)

%20(1).avif)

Frequently Asked Questions

1. What are some advantages of utilizing the marketplace?

Employees can choose from dozens (sometimes hundreds, depending on zip code) of plans. These plans are often less expensive compared to group plans. In short, employees get exponentially more options for less money.

2. Where do we look for our locally offered plans?

It will depend on the state that you’re in. For the federal exchange, you will look at healthcare.gov. Some states also host their own state-based exchanges. Vitable will meet with each employee to help them navigate their local marketplace and recommend the best health insurance for their unique situation.

3. Can I claim tax deductions for my HRA contributions?

Your HRA contributions are entirely tax-deductible. This financial advantage adds to the appeal of utilizing HRAs for healthcare coverage. Additionally, the funds directed to employees' HRAs do not need to be reported as income, effectively offering them tax-free financial support for their medical expenses.

4. How does the tax treatment of HRA contributions benefit employees?

HRA contributions offer a significant tax advantage, as they are 100% tax-deductible. Moreover, the funds allocated to employees' HRAs do not count as taxable income, providing them with tax-free resources designated for their medical necessities.

5. Are health insurance exchanges solely government-operated?

The term "health insurance exchange" predominantly signifies government-created public exchanges, a response to the Affordable Care Act. These platforms streamline the acquisition of individual and family health insurance plans that align with ACA stipulations.

Book your consult with Vitable

Our team knows the ins and outs of the health insurance marketplace and will guide you towards the solution that makes the most sense for your business and your team. Come with questions! Our experts are happy to dig into the details to get you the clarity you need.

During the call, Vitable will run a cost-benefit analysis on your company's current healthcare spending and show you different ways you can save—without sacrificing plan quality. After your consultation, Vitable will design a unique plan for your employees’ health insurance, including suggested plans and accounts, plan policy documents, and the annual budget. Book Your Call Here.

Understanding Health Insurance Exchanges

A health insurance exchange, often called a health insurance marketplace, is a hub for comparing and selecting health insurance options. Here, private health insurance companies showcase their plans, allowing individuals to make informed comparisons among available offerings.

The term "health insurance exchange" commonly denotes government-created public health insurance exchanges, a response to the Affordable Care Act (ACA). These public exchanges are instrumental in facilitating the purchase of individual and family health insurance plans that align with ACA regulations. The phrase "individual and family" refers to health insurance that individuals obtain independently, separate from the coverage offered by employers or government programs like Medicare or Medicaid.

As of 2025, several states have transitioned from the federal marketplace to their own state-based exchanges (SBEs). Below is a list of the SBEs and SBEs on the Federal platform (SEB-FPs) for Plan Year 2025:

- SBEs: California, Colorado, Connecticut, District of Columbia, Georgia, Idaho, Kentucky, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Jersey, New Mexico, New York, Pennsylvania, Rhode Island, Vermont, Virginia, Washington

- SBE-FPs: Arkansas, Illinois, Oregon

- States seeking to transition to SBE for Plan Year 2026: Illinois

New Premium Tax Credit Rules for 2025

The Internal Revenue Service (IRS) introduced new updates for individuals relying on premium tax credits to afford health insurance through government exchanges. These changes came into effect for tax years beginning on or after January 1, 2025, and will primarily affect taxpayers who:

- Enroll themselves or family members in health insurance through a government exchange.

- Depend on premium tax credits to lower insurance costs.

The IRS has introduced several updates to the Premium Tax Credit (PTC) rules for 2025 to support consistent implementation of the Affordable Care Act. These include a clarified definition of a “coverage month,” which now refers to any month in which an individual is enrolled in a Qualified Health Plan (QHP) through an Exchange as of the first day of the month, has paid their share of the premium by the due date of their tax return, and is not eligible for other minimum essential coverage. The IRS has also issued guidance on partial premium payments, allowing individuals to remain eligible for tax credits as long as their portion of the premium is paid by the tax return deadline. Additionally, the new rules outline when individuals enrolled in a QHP are considered ineligible for state-run health programs like the Basic Health Program. These updates aim to simplify eligibility and ensure access to premium tax credits remains fair and transparent. For more details, visit IRS.gov.

Explore employee health insurance enrollment, tax credits for HRAs, and the world of health insurance exchanges in this comprehensive guide.

How Employees Purchase Individual Health Insurance

With the help of Vitable Health and our broker partners, the enrollment process for employees is quick and straightforward. A member of the Vitable team will meet with each of your employees individually, virtually, or in person. After providing their age, zip code, household income, smoking status, and spouse/dependent’s ages, the Vitable expert will walk them through their top three plan recommendations, helping them find the best plan for them and their lifestyle. The employee will then enroll in health insurance online, either on healthcare.gov for the federal exchange or on a state-based website for the state exchange.

A main factor employers must consider is that the Individual Coverage Health Reimbursement Arrangement (ICHRA) is not a group plan, so employees will be subject to group banding. However, since the ICHRA is customizable, you can set age bands. For example, your older employees' health insurance premiums will be more expensive, and you can offer them a higher reimbursement limit than younger employees. Although there is no age banding on traditional group health insurance, your employees’ age impacts the group health premiums.

Tax Credits for HRAs

Your HRA contribution is 100% tax-deductible. Also, the money you put in your employees’ HRA is not reported as income, so they get tax-free money for their medical needs.

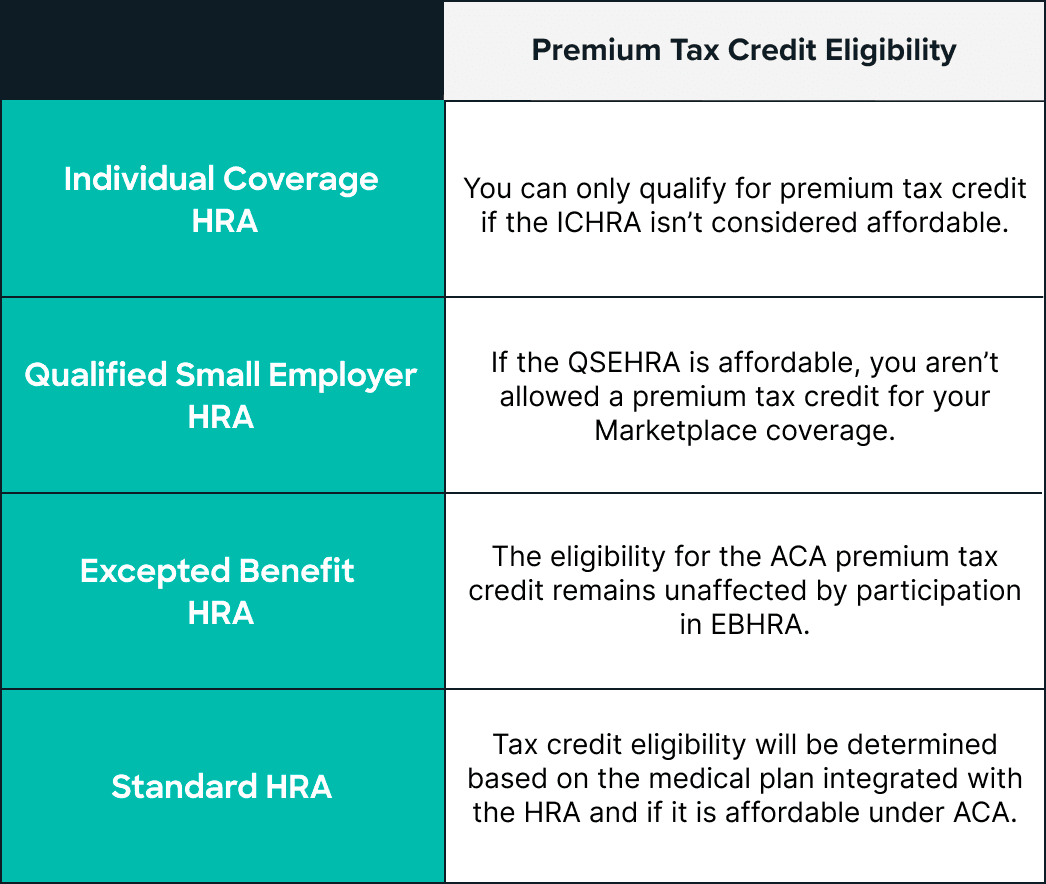

Standard HRA

Those offered a Standard HRA may still qualify for premium tax credits for Marketplace coverage under the ACA. Tax credit eligibility will be determined based on whether the significant medical plan integrated with the HRA is “affordable” under ACA rules.

ICHRA

An individual coverage HRA offer may impact your eligibility for the premium tax credit for Marketplace coverage. The only way you’ll qualify for the premium tax credit to help pay for Marketplace coverage is if you don’t accept the individual coverage HRA, and the individual coverage HRA isn’t considered affordable. For 2025, employees' share of health insurance premium costs cannot exceed 9.02% of their household income.

If the HRA is considered “affordable,” and you accept the HRA, you aren’t eligible for the premium tax credit for your Marketplace coverage. If the HRA includes payments to cover the expenses of your household members, you can’t get a premium tax credit for your household members.

Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

Tax credits differ for each HRA type, but for a QSEHRA, you may be eligible for some or no tax credit, depending on whether the QSEHRA is affordable. The 2025 QSEHRA guidelines through Revenue Procedure RP-2024-401 limits will be $6,350 for self-only coverage and $12,800 for family coverage. Reimbursements may be applied toward eligible healthcare expenses as outlined under IRS Section 213(d). To ensure these reimbursements remain tax-exempt, employees must have Minimum Essential Coverage (MEC) in place.

Excepted Benefit HRAs (EBHRA)

The eligibility for the ACA premium tax credit remains unaffected by participation in EBHRA. This applies even to EBHRAs that reimburse eligible medical expenses and cost-sharing, which are not covered by individual health insurance. For plan years beginning in 2025, the maximum amount that may be made newly available for the plan year for an EBHRA under §54.9831-1(c)(3)(viii) is $2,150.

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.