.avif)

Table of Contents

Related Blogs

.avif)

%20(1).avif)

Picking a health plan for your team is one of the biggest decisions you'll make all year. Two of the most common options are fully insured plans and self-funded plans. But what's the difference? And which one makes sense for your business?

This guide breaks it all down in plain language, backed by recent data.

Why This Decision Matters More Than Ever

Health insurance is getting expensive fast.

According to KFF's 2025 Employer Health Benefits Survey, the average employer-sponsored family premium hit $26,993 in 2025. That's a 26% increase over the last five years, faster than the rate of inflation.

Employers are feeling squeezed. And more of them are looking at alternatives to traditional fully insured plans.

Here's what the data shows: 67% of covered workers in the U.S. are now in self-funded health plans, according to KFF's 2025 survey. That includes 80% of workers at large firms and a growing share of small businesses, too.

So what does that mean for you? Let's start with the basics.

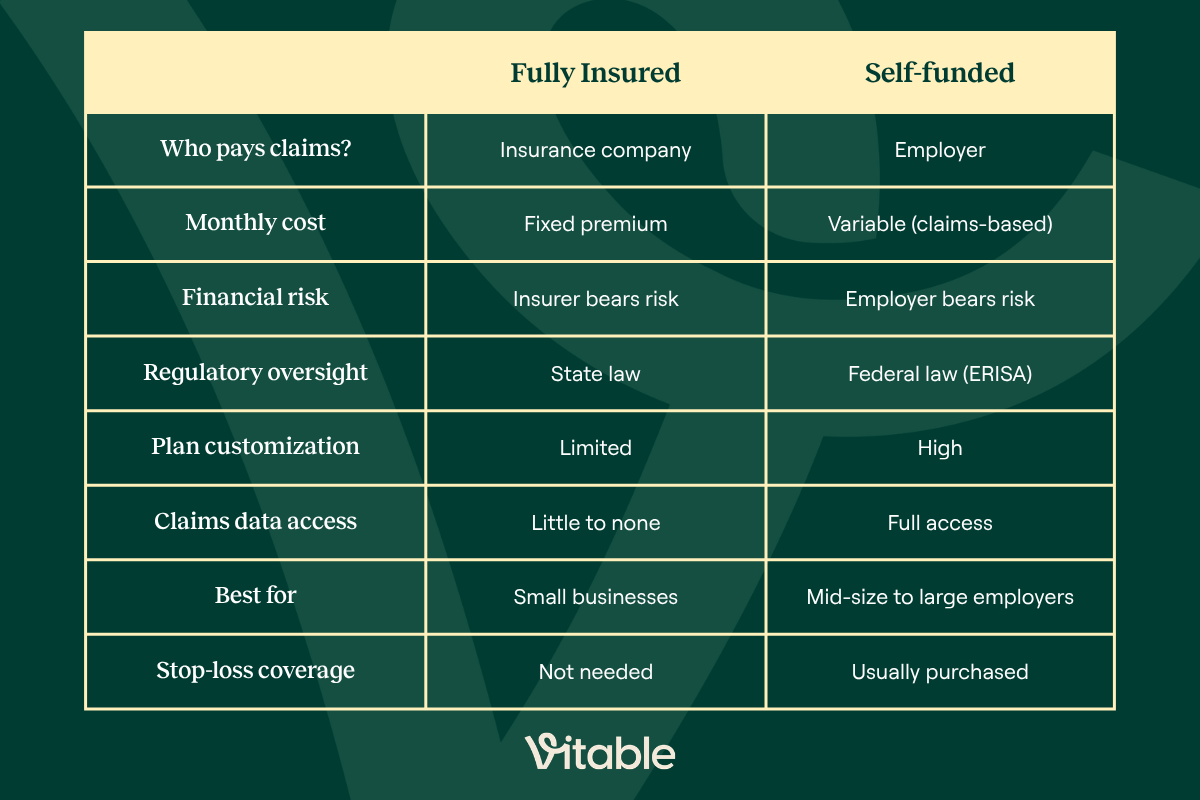

What Is a Fully Insured Health Plan?

A fully insured plan is the traditional way employers buy health coverage.

You pay a fixed monthly premium to an insurance company. The insurer covers your employees' medical claims. You know exactly what you'll pay each month during your plan year—no surprises.

The insurer takes on all the risk. If your employees have high claims throughout the year, the insurer absorbs the cost of those claims. If they have low claims, the insurer keeps the difference between the premiums you pay in and the claims they pay out.

Key features of fully insured plans:

- Fixed monthly premiums

- Regulated by state insurance laws

- Insurance company pays all claims

Fully insured plans are common among small businesses. They're simple and predictable, but that simplicity can come at a cost.

What Is a Self-Funded Health Plan?

A self-funded health plan (also called a self-insured plan) works differently.

Instead of paying an insurance company take on the risk of covering employee claims, you pay your employees' medical claims directly. You set money aside each month to cover those costs. When an employee gets care, you pay the bill.

Most self-funded employers partner with a third-party administrator (TPA). The TPA handles paperwork, processes claims, and manages day-to-day operations. But the financial responsibility stays with you.

To protect against catastrophic claims, most self-funded employers also buy stop-loss insurance. This kicks in when costs spike above a set threshold.

Key features of self-funded plans:

- You pay claims directly

- Costs vary month to month based on actual claims

- Federal law (ERISA) governs the plan, not state law

- More control over plan design

- Full access to your own claims data

Self-Funded vs. Fully Insured: Side-by-Side Comparison

How Does Self-Funded Insurance Work?

To understand how self-funding works, let's look at an example.

Say you run a company with 150 employees. Under a fully insured plan, you might pay $700 per employee per month toward insurance premiums. That's $105,000 per month, no matter what happens.

Under a self-funded plan, you set aside $580 per employee based on expected claims. If your employees are healthy, you spend less. If claims spike, you spend more.

If you have stop-loss insurance and your employee claims spike above a certain dollar amount, that's where it kicks in. It caps your exposure beyond your stop-loss limit. So, if you set a specific stop-loss limit at $50,000 per person per year. and an employee exceeds that, your liability is capped. The stop-loss carrier covers the rest.

Here's the basic flow:

- Employee gets medical care

- Provider sends the claim to your TPA

- TPA processes the claim and pays the provider

- You reimburse the TPA from your claims fund

- Stop-loss coverage kicks in if costs exceed your threshold

The key insight: in a good year with few claims, excess money stays with you. In a fully insured plan, the insurer keeps it.

Is Self-Funded Insurance Good for Employees?

This is one of the most common questions, and a fair one.

For employees, the day-to-day experience often looks identical to a fully insured plan. They still get an insurance card. They still visit their doctors. Claims still get processed.

But there are real differences worth knowing.

Potential benefits for employees:

- Plans can be customized to cover specific needs, like better mental health benefits, fertility coverage, or direct primary care

- Employers have a direct incentive to invest in wellness and prevention because healthier employees mean lower claims

- No state-mandated benefit requirements, which can allow for more creative or generous plan design

- You could use your claims data to lower deductibles and out-of-pocket costs for employees

Potential drawbacks for employees:

- Benefits can change more often, since the employer controls the plan

- Fewer state-level consumer protections

- If the employer doesn't manage the plan well, employees may see worse coverage

- One or a number of unhealthy employees could lead to higher premiums or reduced benefits for all employees

Overall, self-funded plans can be excellent for employees, especially when the employer uses the flexibility to build a better plan rather than just cutting costs.

Pros and Cons for Employers: Fully Insured Plans

Pros

- Predictable costs. You know exactly what you'll pay each month during your plan year.

- Less administrative work. The insurance company handles everything. You just pay your premium.

- Lower financial risk. If your team has a rough health year, you're not on the hook for extra costs.

- State consumer protections apply. State insurance laws protect your employees in ways ERISA may not.

Cons

- You pay whether claims are high or low. A healthy year and a sick year cost you the same. The insurer keeps the difference.

- Limited customization. You choose from plans the insurer offers. You can't easily tailor benefits to your workforce.

- No claims data. You can't see where your health care dollars go, or take action to reduce costs.

- Annual premium increases. KFF data shows employer premiums have jumped 26% over five years. Fully insured employers have little leverage to push back.

Pros and Cons for Employers: Self-Funded Plans

Pros

- Lower costs in good years. Pay for what your employees actually use—not what an insurer assumes they might use.

- Full plan design control. Build a plan that fits your workforce. Add direct primary care, customize deductibles, or focus on high-value providers.

- Access to your claims data. See exactly what's driving costs and take action. This data is one of the most valuable tools in managing long-term benefits spending.

- Exempt from state insurance mandates. Because self-funded plans fall under ERISA, you don't have to comply with state-specific rules. This matters a lot for employers with workers across multiple states.

Cons

- Financial risk. A bad claims year can be costly. Stop-loss insurance helps, but adds cost.

- More complexity. You need a good TPA, a claims fund, and more administrative bandwidth.

- Cash flow demands. You need money available to pay claims as they occur, which can strain smaller employers.

One Way to Reduce Claims: Add Primary Care

Here's something many employers don't realize: a major driver of high claims is employees who can't access timely primary care.

When employees skip a doctor visit because of cost or access, small problems become big ones. A missed blood pressure check becomes a stroke. A skipped annual exam becomes a late-stage cancer diagnosis. Both are devastating for the employee, and very expensive for your self-funded plan.

That's where employer-sponsored primary care comes in.

A growing number of self-funded employers are adding a direct primary care membership—like Vitable Primary Care—as a layer on top of their health plan. For a flat monthly fee per employee, every worker gets unlimited access to everyday care. No copays, no deductibles, no barriers. Adding this enhancement can reduce overall health costs for both employers and their employees.

The data backs this up. An independent actuarial analysis by Windsor Strategy Partners—a healthcare actuarial firm serving self-funded plans, captives, and insurers—found that Vitable Primary Care reduces aggregate claims by an average of 10.1%.

The analysis modeled reductions of 20% in ER utilization, 50% in urgent care visits, and 50% in primary care claims–all redirected to Vitable Primary Care.

For self-funded employers, this can have a significant financial impact. Every claim you don't pay is money that stays in your plan fund.

What Other Health Plan Funding Models Exist?

If a fully insured plan sounds too rigid, but self-funding sounds too risky, there are other options. We'll cover two of them below.

Level-Funding

With both self-funding and level funding, you take on more risk than a fully insured plan. But the two have some key differences.

With self-funding, you own your claims fund and pay claims directly as they come in. Stop-loss insurance kicks in if any one claim—or your total claims—cross a set threshold. If it's a healthy year and claims stay low, you keep every dollar that's left.

With level funding, you pay a fixed monthly premium to a carrier or TPA, like you would with a fully insured plan. The carrier or TPA holds your funds in a separate account and uses them to pay claims and cover stop-loss premiums. If claims come in lower than expected, you may get a refund at year-end.

Think of it this way: with self-funding, the money is yours until you spend it. With level funding, you're handing it to someone else to manage and hoping to get some back.

According to the 2025 KFF survey, 37% of covered workers at small and mid-size firms are now enrolled in level-funded plans. These plans are one of the fastest-growing options in the market because they make self-funding accessible to smaller employers.

The Individual Coverage Health Reimbursement Arrangement (ICHRA)

There's one more option worth knowing about, especially if you want maximum cost predictability with minimum claims risk.

An ICHRA lets you give employees a fixed monthly allowance to buy their own individual health insurance—the same fully insured, community-rated plans available on the ACA Marketplace.

Here's why this is a big deal:

- Your costs are 100% fixed. You set the allowance. You never pay more.

- Employees enroll in individual, fully insured plans. That means they're protected by all ACA consumer rules, and their premiums are based on community ratings, not your group's claims history.

- You're technically self-funding—but without claim volatility. With an ICHRA, you provides employees monthly allowances. However, because you define that allowance, employees cannot exceed that dollar amount. There are no surprise claims, and no renewal shocks based on your employees' health.

ICHRA adoption is growing fast. According to the HRA Council, ICHRA adoption grew 34% among large employers from 2024 to 2025, and 18% among small employers. More than 83% of employers that adopted an ICHRA in 2025 hadn't previously offered health coverage at all.

Vitable Health administers ICHRAs for employers who want the predictability of a defined contribution with the flexibility to offer employees individual market choice—and the ability to layer on additional benefits like primary care.

Which Plan Is Right for Your Business?

The right choice depends on a few key factors.

Consider a traditional self-funded plan if:

- You have 100 or more employees

- You have a relatively healthy workforce

- You want full control over plan design

- You want access to claims data and a long-term cost management strategy

Consider a level-funded plan if:

- You have 10–99 employees

- You want the benefits of self-funding (data access, refund potential, flexibility) with more predictable monthly costs

- You're not ready to absorb catastrophic claims risk directly

Consider an ICHRA if:

- You want 100% cost predictability — no claims risk at all

- You have employees in multiple states and want to avoid managing a multi-state group plan

- You want employees to have individual plan choice rather than a one-size-fits-all group plan

- You're a smaller employer who previously couldn't afford group coverage

Consider a fully insured plan if:

- You're a very small employer (under 10 employees) with limited administrative bandwidth

- You need the simplest possible benefits structure

- Your workforce has significant health conditions that could make self-funding expensive

Key Takeaways

- Fully insured plans offer predictability but limit customization, data access, and cost savings.

- Self-funded plans let employers pay for actual claims, access their data, and potentially save money, but carry more financial risk.

- Level-funded plans combine fixed monthly payments with the upside of self-funding, and are growing fast among small businesses.

- ICHRA is technically a form of self-funding, but with zero claims risk. Employers set a fixed allowance and employees buy their own fully insured plans.

- Adding primary care, like a Vitable Primary Care membership, reduces claim volume for self-funded employers.

- The right choice depends on your company size, workforce health, risk tolerance, and administrative capacity.

Want to explore whether a self-funded, level-funded, or ICHRA plan is right for your team— and whether adding Vitable Primary Care could reduce your claims? Talk to a Vitable Health advisor.

Frequently Asked Questions

What is the difference between self-funded and fully insured health plans? In a fully insured plan, you pay a fixed premium and the insurer covers all claims. In a self-funded plan, you pay claims directly and take on more financial risk, but also get more control and can save money when employees are healthy.

What is self-funded health insurance? Self-funded health insurance is a plan where the employer pays employees' medical claims. Most employers buy stop-loss insurance to protect against high-cost claims and work with a TPA to manage day-to-day administration.

Is self-funded insurance good for employees? It can be. Employees often get more personalized benefits and better wellness support. The key is whether the employer uses the flexibility to build a better plan and not just cut costs.

How many employees do you need to self-fund? Traditional self-funded plans work best for 100 or more employees. Level-funded plans make self-funding accessible for employers with as few as 10–25 employees.

What is a level-funded health plan? A level-funded plan is a hybrid option. You pay fixed monthly amounts like a fully insured plan, but if actual claims come in under budget, you get a refund at year-end.

What is an ICHRA and how does it relate to self-funding? An ICHRA is a type of self-funded benefit where the employer sets a fixed monthly allowance and employees use it to buy their own fully insured individual plans. Unlike traditional self-funding, there are no claims to manage and no surprise costs.

Can I add primary care to a self-funded plan? Yes, and it's one of the smartest ways to reduce claims. Employer-sponsored primary care memberships remove barriers to routine care, which prevents the costly ER visits and hospitalizations that drive up self-funded plan costs.

Sources

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.