Table of Contents

Related Blogs

.avif)

%20(1).avif)

Why Vitable Is a Better Employee Health Benefit Solution for Small Businesses

Looking for a smarter way to manage your small business medical benefits? Vitable is an affordable health benefits platform that offers several comprehensive employee benefit plans tailored for small businesses, combining flexibility with simplicity.

Employers can choose from innovative coverage options including ICHRA, QSEHRA, and MEC + Minimum Value Plans, all of which all come standard with Vitable’s DPC membership. For a flat monthly fee, DPC through Vitable provides employees with convenient same-day or next-day access to primary care services without the hassle of copays or deductibles.

Our dedicated experts offer personalized support from real people without the frustrating call center experience. With our integrated DPC services, you ensure your employees are happy without the administrative burden of insurance claims. Simply put, we’re built for making healthcare better for businesses.

Ready for Better Small Business Medical Benefits?

Small business medical benefits don’t have to be complicated. There are better, more flexible options like ICHRA, QSEHRA, and MEC + DPC plans that can help you take control of your company’s healthcare spending without breaking the bank.

Combining Vitable’s ICHRA and DPC offers easy-to-use health reimbursement accounts with convenient access to virtual primary care providers with no copays, no deductibles, and no hassle. Your team gets quality healthcare when they need it without worrying about complex paperwork or unexpected bills, while you benefit from Vitable’s HRA administration expertise to keep your small business running smoothly.

Want to learn how we can create a health benefits plan that works for your company? Fill out the form below!

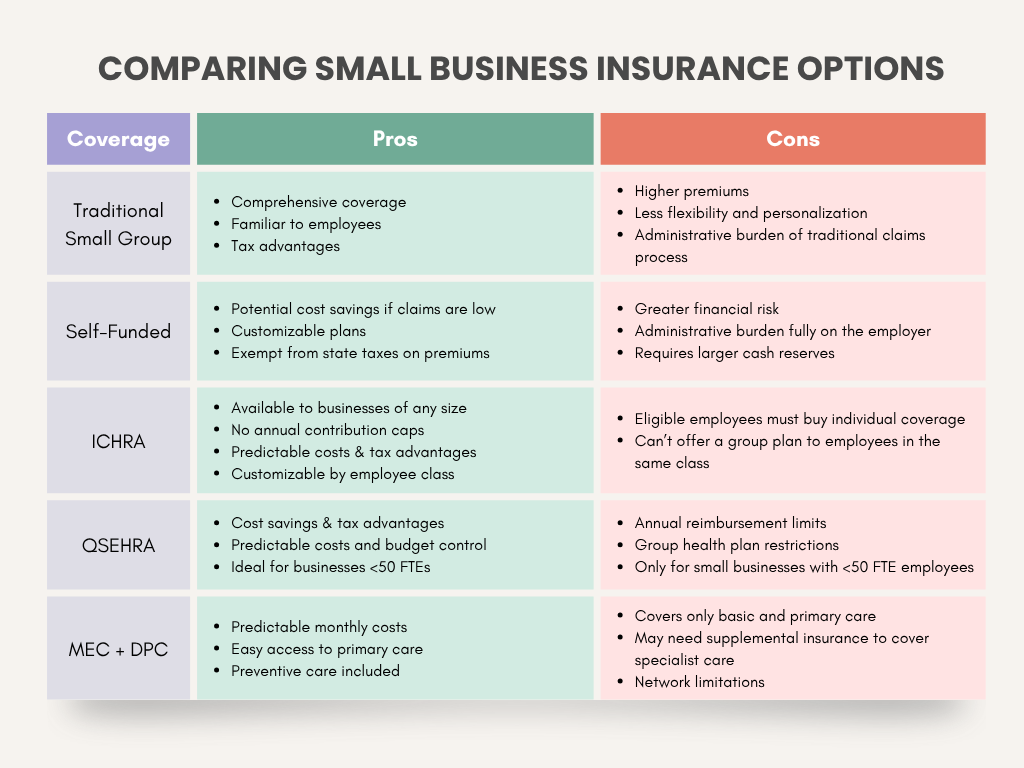

4. MEC + DPC Membership

Pairing a Minimum Essential Coverage (MEC) plan with a Direct Primary Care (DPC) membership gives small businesses a cost-effective way to meet ACA requirements and provide employees with real, everyday healthcare they’ll actually use.

MEC plans satisfy Part A of the Employer Mandate by covering essential preventive services like annual checkups, vaccines, and screenings. But on their own, MEC plans don’t cover the full range of care most employees need.

That’s where DPC comes in. For a flat monthly fee, DPC provides unlimited access to primary care, including same-day or next-day visits, routine care, chronic condition management, mental health support, and more — without copays, deductibles, or insurance claims.

Read more here about how this combined approach works — and why it’s gaining traction with small businesses.

Table 1. Comparing Top Small Business Medical Insurance Options to Offer Affordable Employee Benefits

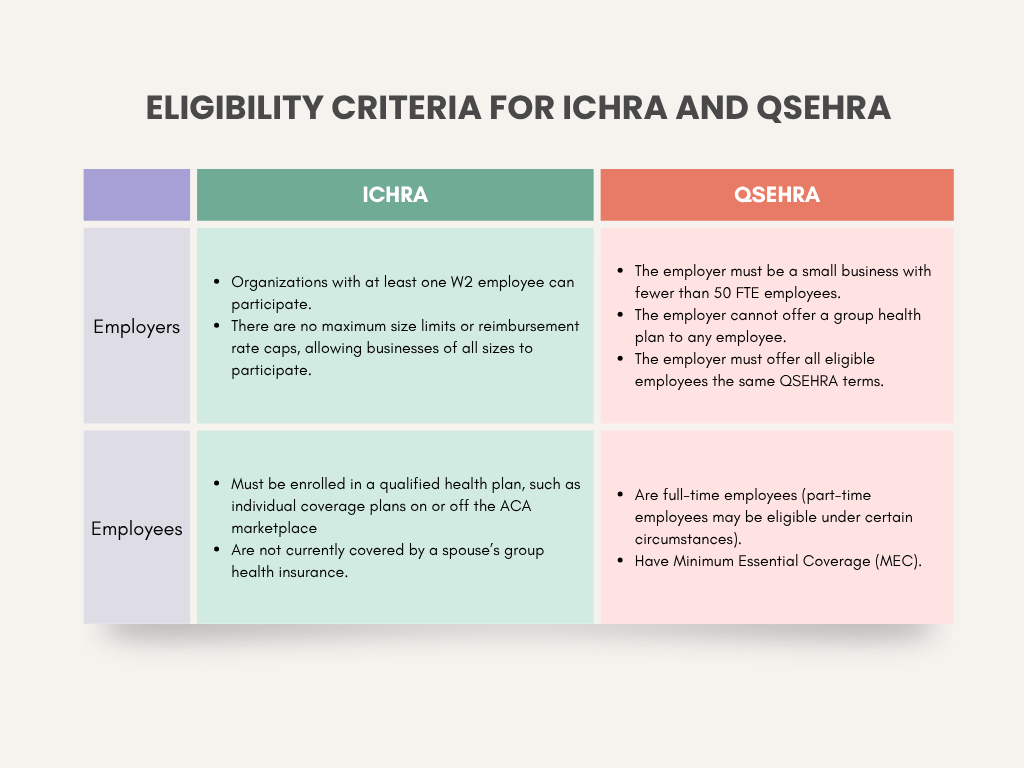

What Is an HRA? ICHRA vs. QSEHRA

HRAs are one of the most flexible and cost-effective ways for small businesses to provide competitive employee health benefits within their budget, while also giving employees more choice and control over their healthcare. Employers provide a set monthly reimbursement allowance, and employees use those funds to purchase their own individual health insurance plans, typically through the ACA Marketplace or a private exchange.

The best HRA options for small business medical benefits in 2025 include the ICHRA and QSEHRA. See Table 2 below to determine if your company and employees are eligible.

- ICHRA: Allows employers of any size to reimburse employees for some or all of the cost of health insurance premiums that they purchase on their own. Learn more about the ICHRA here.

- QSEHRA: Explicitly designed for small businesses with fewer than 50 full-time or FTE employees to provide tax-free reimbursements for eligible medical expenses. Learn more about the QSEHRA here.

Table 2: Key eligibility criteria for employers and employees for ICHRA and QSEHRA

Both these HRAs are valid options when offering small business medical benefits, but because the ICHRA has no company size restrictions or annual contribution limits, it offers the greatest customizability and scalability for a variety of businesses. Employers can vary reimbursement amounts by employee class (such as full-time vs. part-time, salaried vs. hourly, or by location) based on their unique workforce needs.

Discover how ICHRA plans through Vitable are offering a smarter, more affordable way for small business employers to provide comprehensive employee health benefits.

Health benefits shouldn’t be a burden, but for small businesses in the United States (U.S.), rising costs and complex regulations are making it harder than ever to offer meaningful coverage. Traditional employer-sponsored health insurance plans continue to grow more expensive, leaving many employers stuck choosing between affordability and access.

According to the annual Employer Health Benefits Survey by KFF, a nonprofit health policy organization, the average cost of employer-provided health insurance increased by 7% for family plans and by 6% for individuals in 2024. Rising healthcare costs, combined with the financial pressure of remaining compliant with healthcare laws such as the Affordable Care Act (ACA), are making it challenging for smaller businesses to maintain affordability in offering small business medical benefits in 2025.

But there’s good news! Innovative, flexible models like Individual Coverage Health Reimbursement Arrangements (ICHRAs), Qualified Small Employer HRAs (QSEHRA), and Direct Primary Care (DPC) are helping small businesses rethink what’s possible, offering real healthcare solutions that are easier to manage and actually serve the needs of today’s workforce.

In this article, we’ll discuss how options like ICHRAs and QSEHRAs can be integrated with Direct Primary Care (DPC) to give your employees better healthcare while protecting your budget. Whether you’re a business owner or an HR leader, we'll walk you through practical solutions for offering affordable small business medical benefits that make sense, helping you find the right approach that works for your company and team.

In this article, we’ll cover:

- Compliance requirements for businesses of different sizes under current healthcare laws and potential penalties for non-compliance.

- Comparisons of traditional group plans versus newer alternatives like HRAs (i.e., ICHRA, QSEHRA) in terms of costs, flexibility, and small business medical benefits.

- Innovative HRA models integrated with Direct Primary Care (DPC) that now offer a comprehensive, cost-effective solution for small businesses and employee benefits.

Small Business Health Insurance: What Are You Legally Required to Offer?

When are companies legally required to provide employee health benefits? The answer will depend on the company’s size. Based on current ACA requirements, if your business has an average of 50 or more full-time or full-time equivalent (FTE) employees in the previous calendar year, you are likely considered an Applicable Large Employer (ALE).

On the other hand, small businesses that have fewer than 50 full-time employees do not qualify as an ALE and are not legally required to provide health insurance under the ACA. However, this doesn’t mean you shouldn’t offer small business medical benefits. As many as 96% of working Americans believe it is important for a job to offer health insurance, according to a 2022 survey conducted by the U.S. Chamber of Commerce.

Employers must remember that a well-rounded benefits package is often the key to attracting and retaining top-performing talent, while boosting job satisfaction and work productivity. These benefits translate to lower employee turnover and potentially higher profits and cost savings over time. Simply put, even if your small business isn’t legally required to offer employee health benefits, not doing so may actually cost you in the long run. This is why more non-ALE companies are choosing to offer small business medical benefits in 2025.

Small Business Medical Insurance Options for 2025

Let's look at the different ways you can provide small business medical insurance to your employees in 2025. Here are the top four approaches to providing employee benefits that can work for your small business.

1. Traditional Small Group Health Insurance Plans

These are employer-sponsored health plans where the company purchases small group health coverage from an insurance carrier for their employees. Employers typically share the premium costs with employees, generally as a pre-tax paycheck deduction.

2. Self-Funded Insurance Models

In this insurance model, employers set aside funds to directly pay for their employees’ healthcare claims instead of paying this amount as premiums to an insurance carrier. In case claims are higher than expected in a year, employers also have to purchase stop-loss insurance.

3. Health Reimbursement Arrangements (HRAs)

Health Reimbursement Arrangements (HRAs) are tax-advantaged accounts funded by employers to reimburse employees for qualified healthcare expenses. Two of the most popular HRA options for small business benefits are the ICHRA and QSEHRA. Below, we’ll compare how each one works and help you determine which is the best fit for your team.

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.