Table of Contents

Related Blogs

.avif)

%20(1).avif)

Practical Tips to Keep Your ACA Compliance on Track

Determining whether your business qualifies as an Applicable Large Employer (ALE) is a crucial step in staying ACA compliant. By understanding how to count both your full-time staff and your part-time employees as Full-Time Equivalents (FTEs), you can confidently assess your responsibilities and avoid unnecessary penalties.

While the calculations can seem complex at first, breaking them down step by step makes the process more manageable. Stay proactive with the following best practices:

1. Don’t Wait to Check Your Numbers.

If your workforce fluctuates or hovers near the 50-employee threshold, reviewing your FTE calculations mid-year—or even quarterly—can help you plan ahead and avoid surprises during ACA reporting periods.

2. Stay Current on IRS Guidance.

ACA rules and thresholds can shift over time. Regularly check for updates from the IRS to ensure your calculations, classifications, and coverage offerings remain compliant.

3. Double-Check Employee Classifications.

Misclassifying employees as independent contractors can lead to costly compliance issues. Review roles carefully to ensure everyone is correctly categorized under IRS guidelines.

4. Keep accurate records and file on time.

Maintain detailed records of employee hours, classifications, benefit offerings, and all steps taken to meet ACA requirements. Additionally, ensure that all required IRS forms, such as Form 1094-C and Form 1095-C, are filed accurately and on time. Thorough documentation and timely reporting not only support compliance but also help protect your business in the event of an audit.

Vitable Health: Your ACA Compliance Partner

If your business is approaching ALE status, or you're already there, Vitable can help take the guesswork out of compliance. Our affordable, flexible healthcare coverage is built to meet the needs of small to mid-sized businesses, while also scaling to support growing teams and diverse workforce needs.

Whether you’re building on an existing benefits plan or starting from scratch, Vitable offers the tools and support you need to create a solution that works for your team and your bottom line.

We help you:

- Stay compliant with ACA requirements by offering coverage that meets federal standards and supports accurate reporting.

- Offer meaningful coverage that your employees will actually use, focused on accessible, high-quality care that’s easy to understand and easy to use.

- Avoid the headaches of traditional insurance with a streamlined experience, transparent pricing, and flexible options that are practical and accessible.

Our approach helps reduce administrative burden, increase employee satisfaction, and simplify compliance, so you can focus on growing your business with confidence.

Deliver better healthcare access and stay ahead of ACA requirements.

Why Do FTEs Matter Under the Affordable Care Act (ACA)?

The ACA introduced the Employer Shared Responsibility Provision, also known as the Employer Mandate, to expand access to health coverage through the workplace. Under this provision, businesses that meet the definition of an Applicable Large Employer (ALE) are required to offer health coverage to their full-time employees (and their dependents) or face potential penalties. To keep the mandate focused on larger businesses with greater administrative capacity, the ACA applies these rules only to employers with 50 or more full-time employees, including full-time equivalents (FTEs).

What Is an Applicable Large Employer (ALE)?

An Applicable Large Employer (ALE) is any business that averaged 50 or more FTEs during the previous calendar year. You do not need to maintain 50+ employees throughout the entire year. If your workforce size met or exceeded the 50-employee threshold in even a single calendar month, your business qualifies as an ALE for the entire following year.

Once your business crosses that threshold, you’re legally required to offer ACA-compliant health insurance to at least 95% of your full-time employees and their dependents. Failure to do so can result in substantial IRS penalties.

Applicable Large Employer Responsibilities Under the ACA

Once your business qualifies as an Applicable Large Employer (ALE), you're required to meet these key obligations to stay compliant and avoid IRS penalties:

- Offer Minimum Essential Coverage (MEC): Provide health insurance that meets the ACA’s MEC standards to at least 95% of full-time employees and their dependents.

- Ensure Minimum Value (MV): The plan must cover at least 60% of total allowed healthcare costs, including inpatient and physician services.

- Maintain Affordability: For 2025, employee contributions for self-only coverage must not exceed 9.02% of household income. Employers using safe harbor methods (based on W-2 wages, rate of pay, or the federal poverty line) can ensure compliance without needing actual household income.

- Complete IRS Reporting

- Form 1094‑C to summarize the coverage offered

- Form 1095‑C for each full-time employee detailing their health plan coverage

- Avoid Employer Shared Responsibility Penalties

- Section 4980H(a) (“Part A Penalty”): Applies if you fail to offer MEC to at least 95% of full-time staff and at least one receives subsidized coverage through the Marketplace.

- Section 4980H(b) (“Part B Penalty”): Applies when you offer coverage, but it’s either not affordable or fails to meet Minimum Value, and an employee receives subsidized coverage elsewhere.

How to Calculate Full-Time Equivalents (FTEs)

The IRS provides a clear and straightforward process for calculating full-time equivalents (FTEs). This method is designed to standardize part-time employee hours, so employers can fairly assess whether their total workforce size meets the threshold for ALE status.

Here’s the formula:

Step 1: Add up all hours worked by part-time employees in a month

Step 2: Divide total part-time hours by 120. (Total part-time hours in a month ÷ 120) = FTEs)

Step 3: Count the number of full-time employees

Step 4: Add full-time employees + part-time FTEs = Total FTEs for that month

Average this monthly total over the past 12 months to determine if you're an ALE.

Whether you're tracking eligibility for benefits or determining your company's reporting obligations under the Affordable Care Act (ACA), understanding how to calculate Full-Time Equivalent (FTE) employees is an essential step for any business working toward ACA compliance. Your full-time staff are not the only factor that determines whether you’re considered an Applicable Large Employer (ALE) under the ACA. If you employ part-time or seasonal workers, their hours can still push your total workforce over the 50-employee threshold, triggering ACA-compliant coverage responsibilities.

In this article, we’ll break down what an FTE employee is and how to calculate FTEs accurately.

What Is a Full-Time Equivalent (FTE)?

A Full-Time Equivalent (FTE) is a standardized way to measure your workforce based on hours worked, rather than just headcount. It allows you to combine the hours of certain employees to determine how many "full-time equivalent" employees your business has. This metric is commonly used for workforce planning, budgeting, and compliance reporting, including determining Applicable Large Employer (ALE) status under the ACA.

Under the ACA, one FTE represents the total hours worked by multiple non-full-time employees whose combined hours are equal to those of one full-time employee. For example, if several part-time employees work enough hours together to match the workload of one full-time employee, they collectively count as one FTE.

We’ll break down how to calculate FTEs in detail later in the article. But first, let’s define the types of employees who are counted when calculating FTEs.

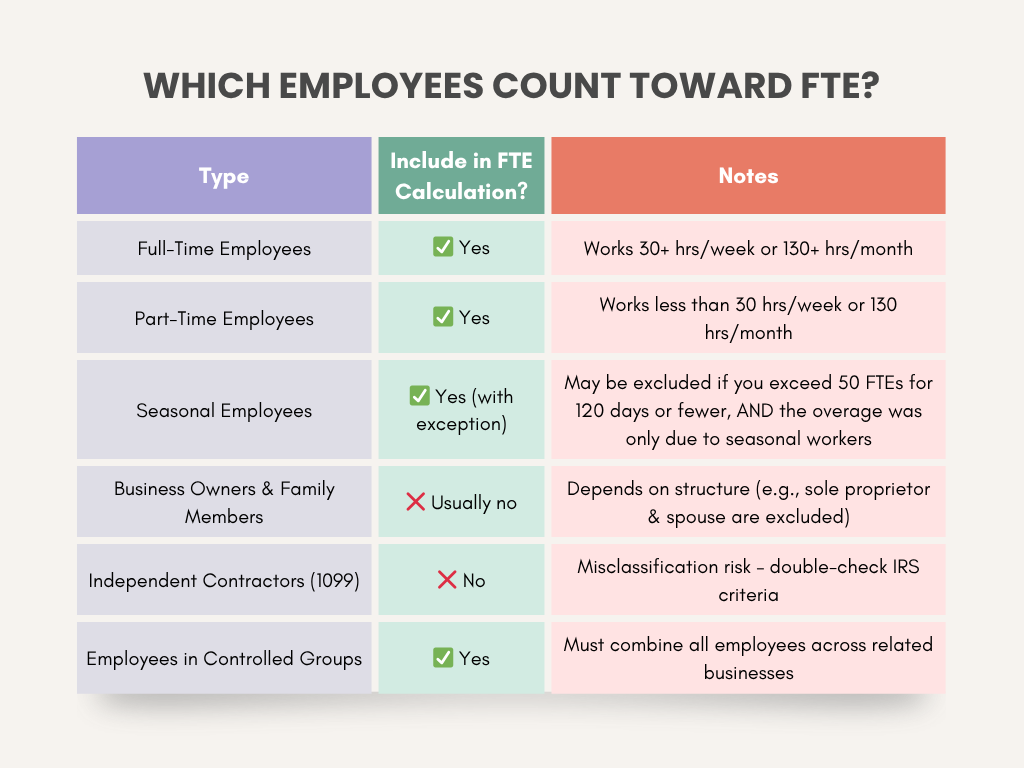

What Types of Employees Count Towards Full-Time Equivalent?

Before you can calculate your total number of Full-Time Equivalents (FTEs), it’s important to know which employees count toward that total. The IRS has clear guidelines on who should and shouldn't be included in your FTE calculations for ACA purposes.

Full-Time Employees

A full-time employee is someone who works 30 or more hours per week, or 130 hours or more in a calendar month. These employees always count toward your total headcount for ACA and FTE purposes.

Part-Time Employees

Part-time employees are those who work fewer than 30 hours per week or less than 130 hours per month. While they aren’t considered full-time, their hours still count toward your total FTE calculation. To calculate their contribution, total all part-time employee hours in a month and divide by 120 (we’ll break this down further later in this article).

Seasonal Employees

Seasonal employees typically work only during specific times of the year (e.g., holidays, summer). Their hours are generally included in your ALE determination, just like full-time and part-time employees. However, there's a specific exception:

You may not need to include season employees in your FTE count if both of the following are true:

- Your workforce exceeded 50 full-time employees (including FTEs) for 120 days or fewer during the calendar year, and

- The employees over the 50-employee threshold were primarily seasonal workers.

If your situation meets both criteria, your business may be excluded from ALE status, even if you temporarily exceeded the threshold.

Business Owners and Family Members

The IRS excludes certain business owners and their family members from FTE calculations, especially in sole proprietorships, partnerships, and S corporations. For example, a sole proprietor and their spouse typically aren’t considered employees for ALE purposes.

If you’re unsure who should be counted based on your structure, consult IRS guidance or a qualified tax advisor.

Independent Contractors and 1099 Workers

Independent contractors are self-employed individuals who receive a 1099 form for tax purposes and are not considered employees, meaning they do not count toward your FTE calculations under the ACA.

Temporary Workers

Temporary workers are employees hired for a specific, short-term period or project, typically through a staffing agency. These employees usually have a defined end date and do not count toward your FTE total because the agency is considered their employer, but if you hire them directly, their hours would count.

Controlled Groups and Aggregated Employers

Controlled groups and aggregated employers refer to two or more businesses that are linked through common ownership or management and must be treated as a single employer under IRS rules. This is especially important when determining ACA responsibilities.

If your business is part of a controlled group or affiliated service group, you are required to combine the total number of full-time and FTE employees across all related entities. Even if no single business in the group has 50 or more employees on its own, the combined count could push the group into Applicable Large Employer (ALE) status.

Failing to account for shared ownership or control can result in compliance issues and unexpected penalties, so it’s important to understand how your organization is structured and how employee counts should be aggregated.

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.