Table of Contents

Related Blogs

.avif)

%20(1).avif)

Keep Clear Records to Prove IRS Compliance

Accurate recordkeeping not only helps you meet ACA reporting requirements, it also serves as your strongest defense in the event of an IRS review or audit. To protect your business from unexpected penalties, it’s essential to document how and when coverage was offered, who was eligible, and what plan details were provided.

Employers should keep clear, organized records of:

- Offer dates and coverage election forms

- Employee status classifications (full-time, part-time, seasonal)

- Measurement period tracking for variable-hour employees

- Plan documents, contribution amounts, and eligibility notices

Vitable simplifies ACA compliance with support services such as: Assistance with IRS Forms 1094-C and 1095-C, open enrollment support, and compliance tracking resources. By leveraging Vitable’s comprehensive services, employers can streamline their administrative processes, reduce the risk of non-compliance, and focus more on their core business operations.

Better Health Benefits Start Here

Increased enforcement, rising healthcare costs, and changing workforce expectations mean employers can no longer afford to treat compliance as an afterthought. With Vitable, you can stay compliant, take care of your employees, and offer better healthcare benefits without stretching your budget or your resources.

Vitable offers affordable benefit plans that satisfy ACA requirements and protect your business from Part A penalties with:

- MEC + Minimum Value Plans: Fully ACA-compliant coverage that includes hospitalization, annual wellness visits, screenings, and other essential services required by the ACA.

- Direct Primary Care (DPC): Unlimited virtual and in-home visits, $0 copays, mental health support, and over 1,000 free prescriptions

- ICHRA Flexibility: Reimburse employees for ACA-compliant individual coverage while controlling costs and customizing benefits by role or location

- Administrative Support: Help with IRS Forms 1094-C and 1095-C, open enrollment assistance, and tools to track eligibility and compliance throughout the year

Take the next step toward better benefits — and partner with a solution designed to make ACA compliance simple, flexible, and employee-friendly.

Key Takeaways

- Part A of the Employer Mandate requires businesses with 50 or more full-time employees (ALEs) to offer Minimum Essential Coverage (MEC) to at least 95% of their full-time workforce and their dependents (biological or adopted children under age 26; spouses are not required to be covered).

- The 4980H(a) penalty is triggered only if an employer fails to meet the 95% requirement and at least one full-time employee receives a Premium Tax Credit to purchase coverage through the Health Insurance Marketplace.

- In 2025, the Part A penalty is $2,900 per full-time employee annually, excluding the first 30 employees. It is assessed monthly at a rate of $241.67 per employee.

- Even short lapses in coverage, such as failing to offer coverage during onboarding or after workforce changes, can trigger the penalty. The IRS treats any period of time during a month (i.e. 1 week) of noncompliance as a full month.

- Accurate employee classification, ongoing eligibility tracking, and timely offers of coverage are essential to maintaining compliance and avoiding costly penalties.

- Proper reporting and recordkeeping, including timely submission of IRS Forms 1094-C and 1095-C, are key to demonstrating compliance and protecting your business from audit risk.

- Employers can meet MEC requirements through ACA-recognized coverage types, including group health plans and ICHRAs paired with ACA-compliant individual insurance.

What Triggers the Part A Penalty?

There are two specific conditions the IRS looks for before a penalty is assessed.

- Employer fails to offer MEC to at least 95% of full-time employees

- At least one full-time employee receives a premium tax credit (subsidy) through the Health Insurance Marketplace.

Stay Ahead of Penalties with the Right Coverage Strategy

Maintaining ACA compliance starts with proactive planning and an effective strategy to protect your business, support your employees, and make healthcare more accessible and sustainable year-round.

Here are three practical strategies employers can use to stay compliant and avoid costly penalties:

1. Offer MEC That Meets ACA Standards

One of the most important steps to avoiding Part A penalties is offering health coverage that qualifies as Minimum Essential Coverage (MEC) to your full-time employees and their dependents. However, MEC doesn’t have to mean minimum value to your team. The right plan can help you stay compliant and deliver real healthcare access that your employees can rely on, without overwhelming your budget or operations.

Vitable’s flexible, compliance-ready benefit solutions make it easier than ever to offer ACA-compliant MEC coverage to your team. With Direct Primary Care (DPC)-based MEC plans and customizable ICHRA options, Vitable gives you the flexibility to meet your ACA obligations while delivering benefits your employees will actually use.

2. Ensure Consistent, Year-Round Coverage

Employers are responsible for ensuring that health coverage is offered consistently throughout the year. Even a brief lapse that causes your coverage rate to fall below the 95% threshold can expose your business to significant ACA penalties. The IRS has zero flexibility when it comes to the 95% coverage requirement. There’s no partial credit or grace period; if coverage isn’t offered or fails to meet ACA standards for any portion of a month, even just a few days, the IRS treats the entire month as non-compliant.

Staying vigilant with workforce changes, onboarding processes, and administrative accuracy is critical to protecting your business from unexpected compliance issues and costly penalties.

Vitable’s workforce-friendly health benefit platform makes it easier to stay ACA-compliant and support your team’s healthcare needs, with built-in tools for eligibility tracking, simple onboarding, and flexible plan structures that help you maintain compliance month after month.

3. Avoid Compliance Pitfalls with Accurate IRS Reporting and Recordkeeping

Offering health coverage that meets ACA requirements is the first step to staying compliant. However, employers must also submit accurate information to the IRS about the health coverage they offer and maintain proper records to back it up.

Each year, ALEs must submit:

- Form 1095-C: Reports on whether full-time employees were offered health coverage and whether it met ACA standards.

- Form 1094-C: A summary form sent to the IRS that outlines the employer’s overall compliance with ACA requirements.

Mistakes, missed deadlines, or incomplete reporting can expose your business to additional IRS penalties, even if you technically met the 95% coverage requirement.

Trying to make sense of ACA compliance can feel overwhelming, especially when it comes to understanding Parts A and B of the Employer Mandate and how they might affect your business. But with the right information, navigating Affordable Care Act (ACA) requirements is far more manageable.

In this article, we’ll break down what the Part A penalty is, how it affects your business, and what you can do to avoid it.

What Is the ACA Employer Mandate?

To help expand access to affordable healthcare, the federal government passed a series of reforms in 2010 collectively known as the Affordable Care Act (ACA). Among these reforms were new requirements for employers, including the Employer Shared Responsibility Provision, commonly referred to as the Employer Mandate. Under the Employer Mandate, businesses that meet the definition of an Applicable Large Employer (ALE) are required to offer health insurance coverage to their full-time employees and their dependents.

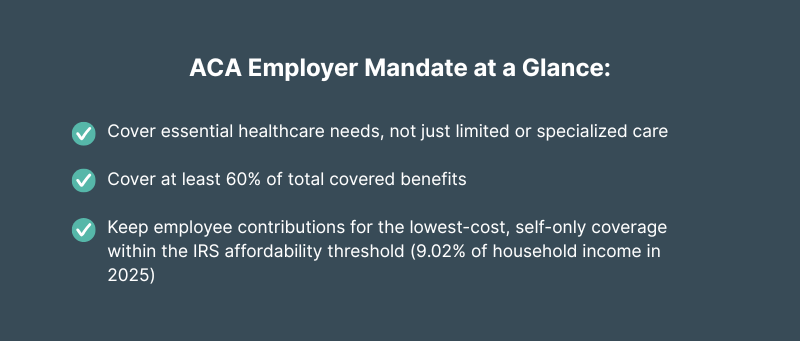

In order to comply with ACA standards, the health coverage offered must meet several key requirements:

- Minimum Essential Coverage (MEC): The plan must provide access to preventive care, emergency services, hospitalization, and other core healthcare benefits.

- Minimum Value (MV): The plan must cover at least 60% of the total allowed cost of covered benefits, so employees are not left responsible for an unreasonably high share of costs through deductibles, copays, and coinsurance.

- Affordability Requirement: To meet ACA standards, the employee’s cost for the lowest-cost, self-only coverage option must not exceed the IRS-set affordability threshold (9.02% for 2025) of their household income. (Note: This percentage is adjusted annually by the IRS.)

Learn more about how to determine if your business qualifies as an ALE here: What is an Applicable Large Employer (ALE)?

What is Part A of the Employer Mandate?

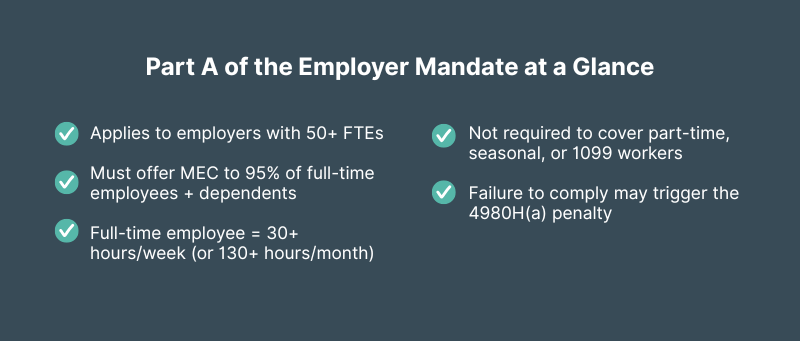

Part A of the Employer Mandate sets the requirement for Applicable Large Employers (ALEs) to offer health coverage that meets Minimum Essential Coverage (MEC) standards to at least 95% of their full-time employees and their dependents (biological or adopted children under age 26; spouses are not included). Failing to meet this requirement can trigger the Part A penalty — officially known as the 4980H(a) penalty.

What Qualifies as Minimum Essential Coverage (MEC)?

Minimum Essential Coverage (MEC) is the ACA-defined minimum level of health insurance coverage that generally includes access to basic medical services such as preventive care, emergency services, and hospitalization. It satisfies the Employer Mandate requirements but does not necessarily include all the benefits of a comprehensive health plan.

Employers can meet MEC requirements by offering one of the following ACA-recognized coverage types:

- An employer-sponsored group health plan, including both small and large group plans

- A grandfathered health plan (in place before March 23, 2010, and has not been significantly altered to reduce benefits or increase employee costs)

- An Individual Coverage Health Reimbursement Arrangement (ICHRA), when paired with an ACA-compliant individual health insurance plan

Learn more about ACA ICHRA requirements here: Your Guide to ICHRA Compliance

Who Must Be Offered Coverage?

The ACA requires that full-time employees and their dependents be offered employer-sponsored health coverage that meets MEC standards.

A full-time employee is defined by the Internal Revenue Service (IRS) as someone who works 30 hours or more per week, or 130 hours or more in a calendar month.

Employers are not required to offer coverage to:

- Part-time employees: Work fewer than 30 hours per week

- Seasonal employees: Work fewer than 120 days in a calendar year

- Independent contractors: Self-employed individuals who provide services to your business (Reported on IRS Form 1099-NEC)

Misclassifying employees or failing to notice when variable-hour workers reach full-time status can quickly drop you below the 95% coverage threshold and trigger costly penalties. Keeping accurate records, tracking employee hours consistently, and offering coverage as soon as someone qualifies is the best way to avoid compliance issues and reduce your risk of the Part A penalty.

What the Part A Penalty Could Cost Your Business

The Part A penalty can add up quickly, especially for larger employers. In 2025, the annual penalty is $2,900 per full-time employee. However, the IRS assesses the penalty amount monthly, not annually. That breaks down to a monthly penalty of $241.67 per full-time employee.

The IRS calculates the penalty based on your total number of full-time employees (minus the first 30 employees), not just the ones you failed to cover.

If you fall below the 95% coverage threshold at any point during the year, and at least one full-time employee receives a premium tax credit through the Marketplace, you could trigger the Part A penalty.

4980H(a) 30-Employee Exclusion

The Employer Mandate includes a provision that allows ALEs to exclude the first 30 full-time employees from the Part A penalty calculation. This buffer helps reduce the financial burden for smaller ALEs.

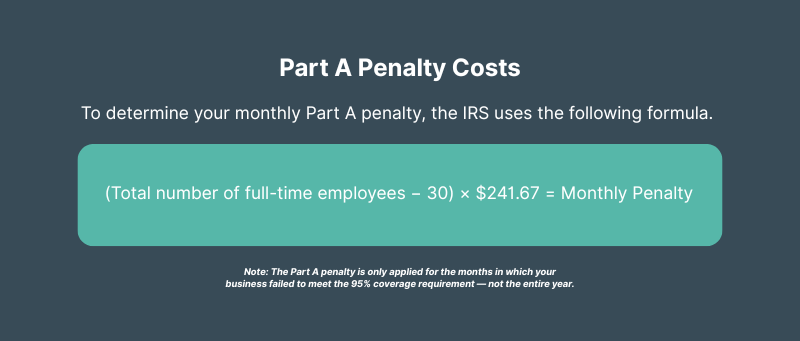

How the Penalty Is Calculated

To determine your monthly Part A penalty, the IRS uses the following formula.

Formula: (Total number of full-time employees − 30) × $241.67 = Monthly Penalty

Note: The Part A penalty is only applied for the months in which your business failed to meet the 95% coverage requirement — not the entire year.

Example:

Let’s say your company has 100 full-time employees and you fail to meet the 95% requirement for three months:

- 100 full-time employees − 30 = 70 employees subject to the penalty

- 70 × $241.67= $16,916.90 per month

- $16,916.90 × 3 months = $50,750.70 total penalty

The part A penalties can add up, but with the right systems in place, staying compliant and avoiding these costs is entirely within reach.

Get a quote

Get a personalized health benefits quote tailored to your company’s unique needs.

Ready to learn more?

Stay ahead with the latest insights on healthcare, benefits, and compliance—straight to your inbox.

Download 2025 Employer Guide to ICHRA

Vitable’s ICHRA Guide gives employers a clear, step-by-step resource for building smarter, ACA-compliant benefits.

This guide explains how ICHRAs work, who qualifies, and how Vitable simplifies setup, onboarding, reimbursements, and compliance — while giving employees more flexibility, control, and care.

Download Vitable’s 2025 Broker’s Guide to ICHRA

The Broker Guide to ICHRAs is a comprehensive resource that helps brokers understand, sell, and manage Individual Coverage HRAs with confidence.

This guide covers everything from compliance and class design to administration flows, case studies, and how Vitable streamlines quoting, enrollments, and reimbursements for brokers, employers, and employees.